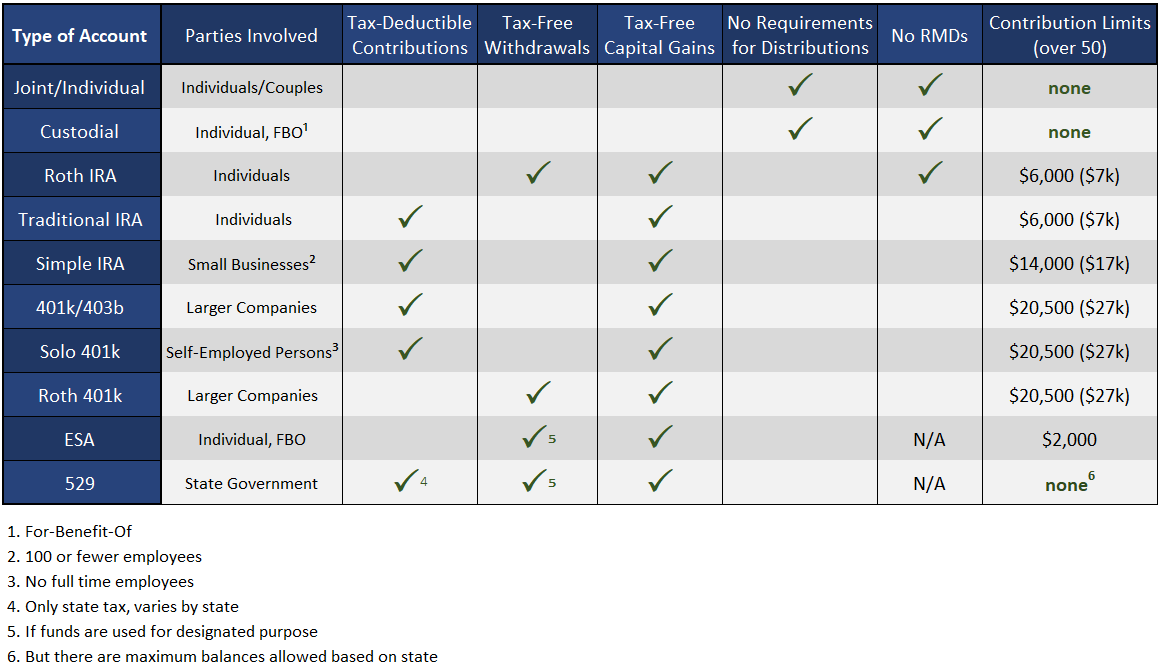

It can be daunting to plan out retirement when there is a seemingly endless number of rules, components, and factors to consider. Because of the complexity of it all, so many put off investing until much later in life, when the greatest potential for long term growth has already passed. As it is important to choose the right option depending on one’s unique financial position, here are the foundational elements of ten different investment accounts that will be discussed in more detail below.

(Numbers for 2022)

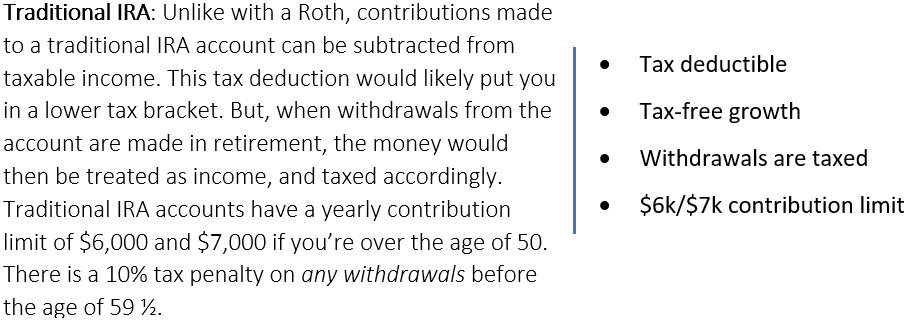

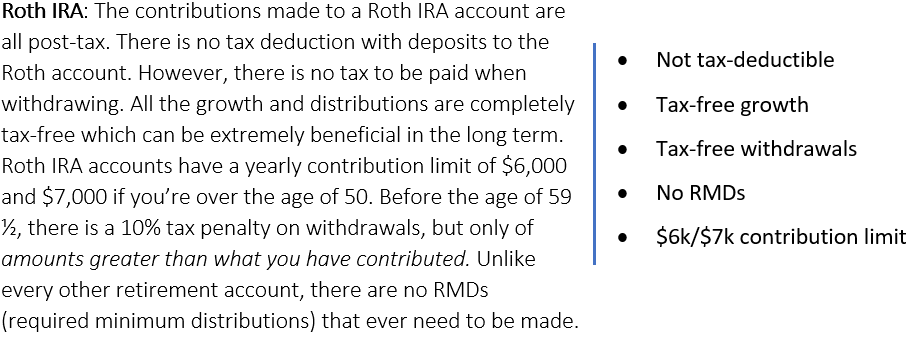

Individual Retirement Accounts (IRAs): Traditional vs. Roth

IRA accounts are the perfect place to periodically deposit money so it can continually invest and grow over many years to make retirement much easier. Most everyone qualifies to open an account and there are few barriers to entry. Here are the main differences between Traditional and Roth IRA accounts to know about:

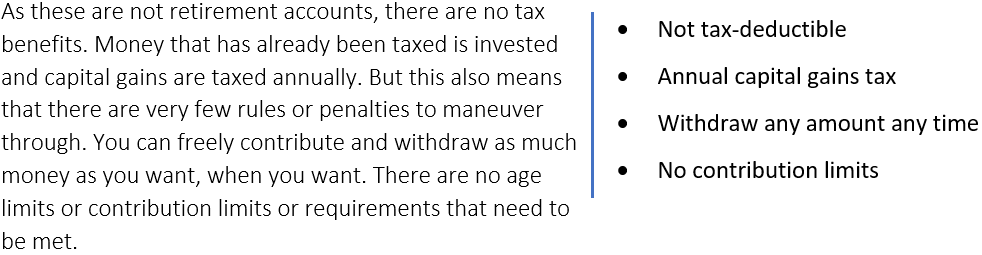

Joint/Individual Investment Accounts

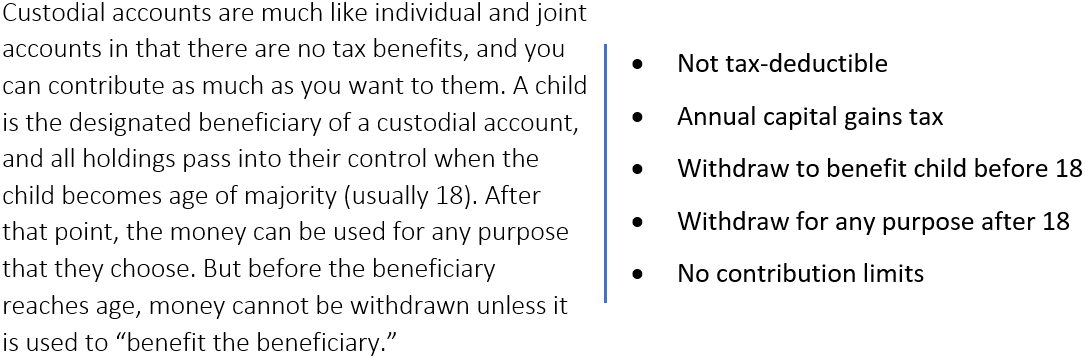

Custodial Accounts

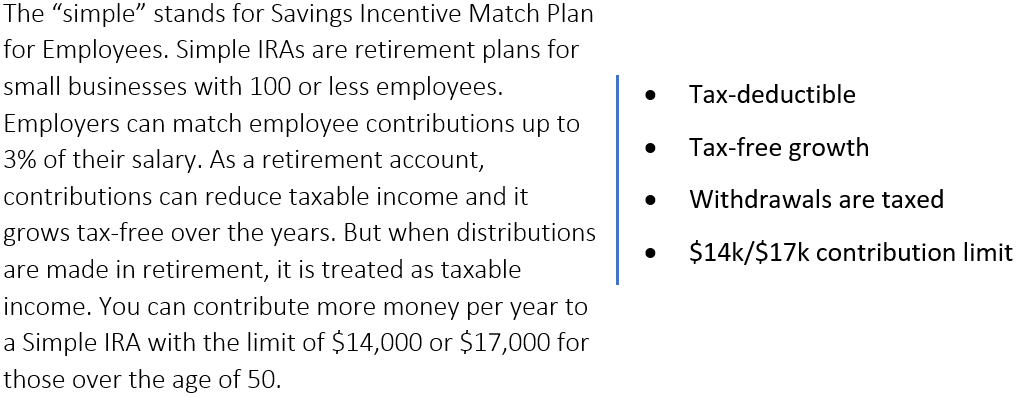

SIMPLE IRAs

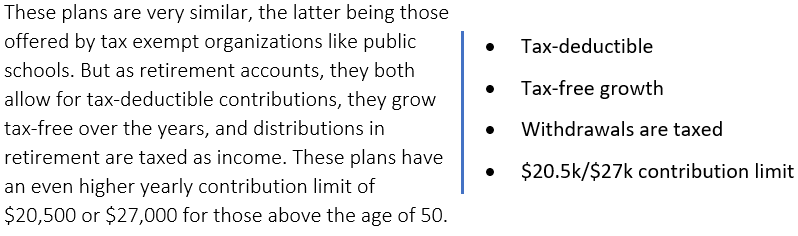

401(k)/403(b)

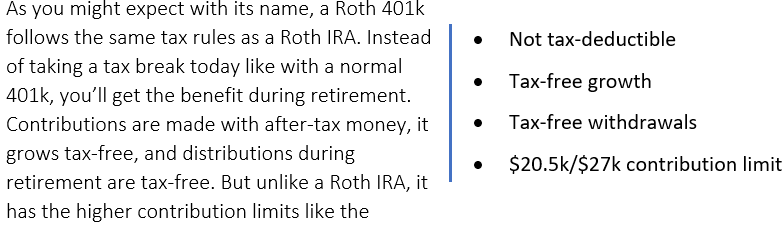

Roth 401(k)

Solo (Roth) 401(k)

These plans have all the same tax and contribution rules as traditional 401ks. But Solo 401ks are made for self-employed business owners who don’t have any other full-time employees. You also have the option to have a Solo Roth 401k plan, which would employ the Roth tax rules.

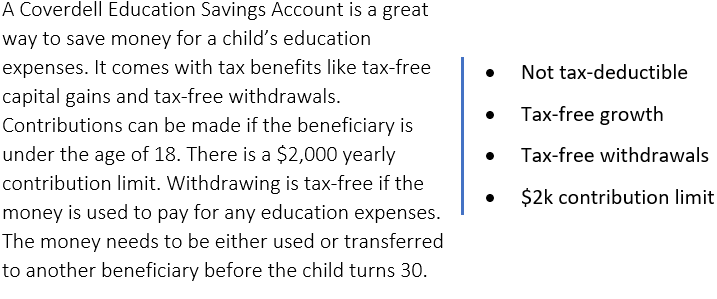

ESA

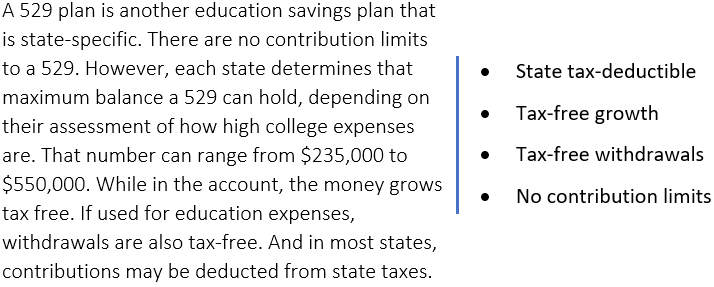

529

“This is a good choice for you if…”

Roth IRA: If you want to consistently contribute money over the long term to an account with major tax benefits that’s separate from any employment or other retirement program.

Traditional IRA: If you want to roll over a previous 401k plan or if you want to have a tax deduction with your contributions now instead of a tax break in retirement.

Simple IRA: If you are the owner or employee of small businesses.

401(k)/403(b): If you are offered this option through your employer.

Solo (Roth) 401(k): If you own a business, have no other employees, and want to contribute much more per year to retirement.

Joint/Individual: If you already max out your plan through work and max out a Roth IRA but want to invest even more.

Custodial: If you want to invest for expenses to benefit your children, or if you want your child to have some money for any use when they reach of age.

ESA: If you want to invest for your child’s education expenses.

529: If you want to invest more than $2,000/year for your child’s education expenses.

By Brenton Walker

References

Kagan, Julia. “Simple IRA .” Investopedia, Investopedia, 26 Nov. 2021, https://www.investopedia.com/terms/s/simple-ira.asp.

O’Shea, Arielle. “529 Plan Rules and Contribution Limits.” NerdWallet, 19 Sept. 2022, https://www.nerdwallet.com/article/investing/529-plan-rules.

Williams, Rob. “Saving for College: Coverdell Education Savings Accounts.” Schwab.com, Charles Schwab, 24 Feb. 2021, https://www.schwab.com/learn/story/saving-college-coverdell-education-savings-accounts