A dollar is worth more today than it is tomorrow, and with the help of compound interest, that couldn’t be truer. This concept is often referred to as the “time value of money” and it shows us that those who are too hesitant to invest their money are in fact, choosing a negative investment.

It seems like discussing retirement is usually reserved for those who are older and approaching the end of their careers. For one reason or another, young people are seldom encouraged to open and contribute to investment accounts while the potential for growth couldn’t be greater.

What is Compound Interest?

To better understand compound interest, we can contrast it with simple interest. With simple interest, you can gain a return on your initial investment over any number of periods. If you invest $1,000 and the return rate is at 5% annually, your account will earn $50 year after year. The growth will be linear. At the end of the first year, your account balance would be $1,050 and increase to $1,100 and the end of the second year, then $1,150, and so on.

On the other hand, compound interest allows the growth to be exponential. The 5% annual return rate is a percentage of the new account balance year after year. The return would increase every year instead of just being the same $50. Because your account balance is higher each year, so is your return. At the end of the first year, your account balance would be $1,050 and increase to $1,102.50 at the end of the second, then $1,157.63, $1,215.51, and so on.

The Power of Starting Early

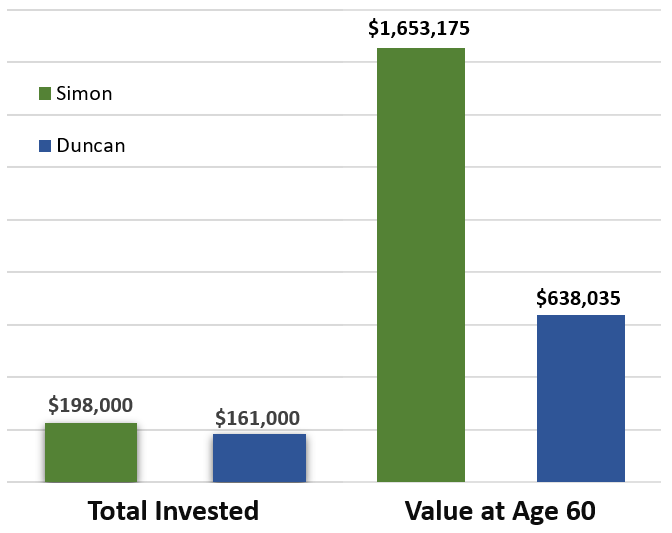

Compound interest can be highly profitable, especially over the long run. To illustrate this, we’ll compare a set of twins, Simon and Duncan, who took slightly different approaches to investing and compare the results when they reach retirement.

Simon decided to begin investing as early and as much as possible. At age 27 he had zero dollars in his IRA but decided to dedicate $6,000 per year until retiring at age 60. Over the 33 years, his highly diversified portfolio had an average annual return of 11%. When he retired at age 60, his IRA’s balance sat at $1.65 million.

Duncan brushed off retirement savings when he was younger. He’s got so much time left, so why worry about it right now? So he opened up his retirement account 10 years later than his brother Simon. At age 37, Duncan began investing $7,000 per year ($1000 more than his twin) and received the same 11% annual return and retired at age 60 just like Simon. But his IRA’s balance only grew to $638,000.

Those 10 years made a difference of over $1 million! From age 27 to 37, Simon only contributed $60,000 but those early contributions made it so that he was over a million dollars richer at age 60. Duncan did very well but could have earned so much more had he simply started a few years earlier.

This chart shows us that the total amount each of them invested was very close. But Simon’s early start gave his money more time to grow, making his balance down the line so much greater. And the huge financial advantage does not end there. During their retirement years, Duncan’s account would continue to grow at about $70,000 per year, while Simon’s account would be earning about $182,000 per year (assuming 11% avg. annual return rate). After 10 years in retirement, Simon will have earned over $1.1 million more than his brother.

The purpose of this example is not to urge anyone to compare their numbers with anyone else’s. We all have unique financial positions. Rather, it is to help us understand the extreme potential in long term compound interest and the colossal effects of putting off investing. “We’re in a recession so it wouldn’t be good to invest when everything is crashing…There’s an election coming up that will crash the market…Stocks have been so green lately, I don’t want to buy in when everything’s high…” We can always come up with reasons to not invest in our futures. But what a mistake it would be to act as the slothful servant who buried his talent out of fear, instead of investing it like his brothers (Matthew 25).

By Brenton Walker

References

“Compounding and the Cost of Waiting.” Compounding and the Cost of Waiting – Wells Fargo, Wells Fargo, https://www.wellsfargo.com/financial-education/retirement/compounding/.